PGNiG on the Stock Exchange

2011 was a year marked by difficult macroeconomic conditions. Many Polish and global stock-exchange indices suffered decline. Therefore, we are all the more satisfied with the performance of the PGNiG share prices, which advanced by more than 14%.

Our Position on the Warsaw Stock Exchange

From the day PGNiG shares were first listed on the Warsaw Stock Exchange, i.e. September 23rd 2005, they have been among the most recognisable and credible listed securities. PGNiG shares have been included in the WIG20 index since December 15th 2005. Our stock is also included in the MSCI Emerging Markets Index, a global index of emerging market companies created by Morgan Stanley Capital International.

PGNiG was, for the fourth consecutive time, listed in the elite group of companies included in the RESPECT Index of socially responsible and sustainable businesses, the first such index in Central and Eastern Europe. Our stock is also a part of the WIG-Paliwa index of fuel sector companies, and of the WIG-div index of listed companies declaring dividend on a regular basis.

| Shareholder | Number of shares/votes attached to the shares as at Dec 31 2011 | Percentage of share capital/total vote at the GM as at Dec 31 2011 | Number of shares/votes attached to the shares as at Dec 31 2010 | Percentage of share capital/total vote at the GM as at Dec 31 2010 |

|---|---|---|---|---|

| State Treasury | 4,272,063,451 | 72.41% | 4,273,650,532 | 72.43% |

| Other shareholders | 1,627,936,549 | 27.59% | 1,626,349,468 | 27.56% |

| Total | 5,900,000,000 | 100.00% | 5,900,000,000 | 100.00% |

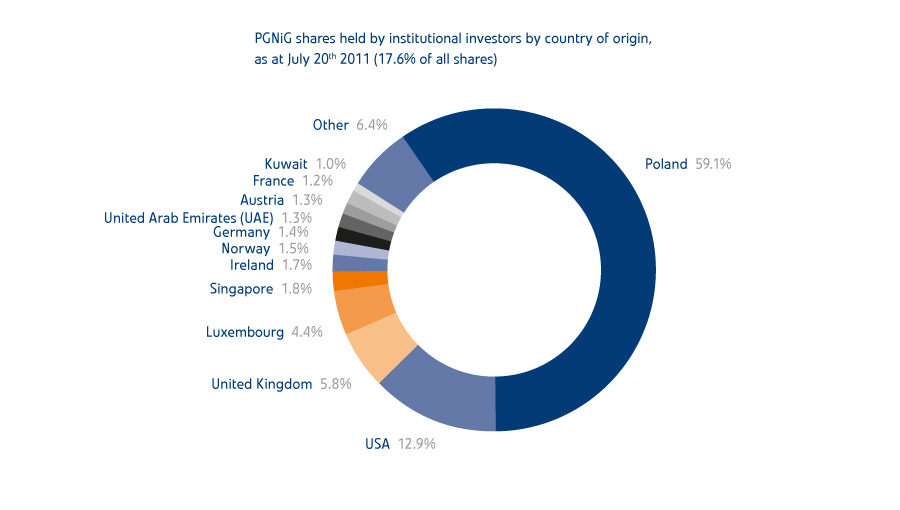

Shareholder Structure

As at December 31st 2011, PGNiG’s share capital amounted to PLN 5,900,000,000 and was divided into 5,900,000,000 shares with a par value of PLN 1 per share. The shares of all series, that is Series A, A1 and B, were ordinary bearer shares and each of them conferred the right to one vote at the General Meeting. The Company’s Articles of Association do not provide for any restrictions on the exercise of voting rights attached to the Company shares.

The State Treasury remains the Company’s majority shareholder. On June 26th 2008, the Minister of State Treasury disposed of one PGNiG share on general terms, which – pursuant to the Commercialisation and Privatisation Act of 1996 – triggered the eligible employees’ rights to acquire free of charge a total of up to 750,000,000 PGNiG shares. The start date for executing agreements on the acquisition of Company shares free of charge was April 6th 2009. On October 1st 2010, the eligible employees’ rights to acquire PGNiG shares free of charge expired.

By December 31st 2011, nearly 60 thousand eligible employees had acquired 727,936,548 shares, which confer the right to 12.34% of the total vote. Consequently, the State Treasury’s interest in PGNiG fell to 72.41%. The shares acquired free of charge by the eligible employees were locked-up until July 1st 2010, while trading in the shares acquired by members of the Company’s Management Board was restricted until July 1st 2011.

Investor Relations

As a company listed on the WSE, PGNiG is required to fairly and reliably report on its operations and important corporate events at the PGNiG Group by preparing and releasing regular reports which are made available on equal terms to each of the Company’s existing and prospective shareholders. Besides interim reports published on a quarterly basis, these include also current reports covering all aspects of the Company’s activities, which could have a material bearing on the share price. The number of such reports increased nearly twofold, from 98 in 2010 to 185 in 2011. Since 2010, the Company has been also publishing corporate governance reports.

The Investor Relations function is, however, not limited to obligatory activities, expressly required by law. It also encompasses various other activities being undertaken by the Company to meet the high expectations of all market participants, which, as a consequence, builds the Company’s reputation and the trust of investors, thereby reducing our funding cost over the long term. These include participation in road shows and investor conferences in Poland and abroad – in 2011, we participated in meetings held in the United Kingdom, Denmark and Austria, and took part in such conferences as “Chemist’s Day – BZWBK” and “ING Annual EMEA Forum” in Warsaw. A new event was the road show promoting the new PGNiG Eurobond Programme, as part of which our representatives held meetings with investors in Paris, London, Amsterdam, Frankfurt, Munich and Vienna.

Investor Relations also involve frequent meetings with portfolio managers in Warsaw and on-going communication with equity analysts covering PGNiG shares. Time-constrained investors expect a condensed and clear approximation of the complex factors having a bearing on the PGNIG valuation. In 2011, the most popular topics of discussions among investors included shale gas plans, acquisition of energy assets, and new hydrocarbon production projects such as the Skarv fields or LMG.

Our website features a dedicated Investor Relations section, where every capital market participant may find the most important updates on the Company, market forecasts of the Group’s performance and the most recent stock recommendations, sourced from research reports by brokerage houses covering PGNiG.

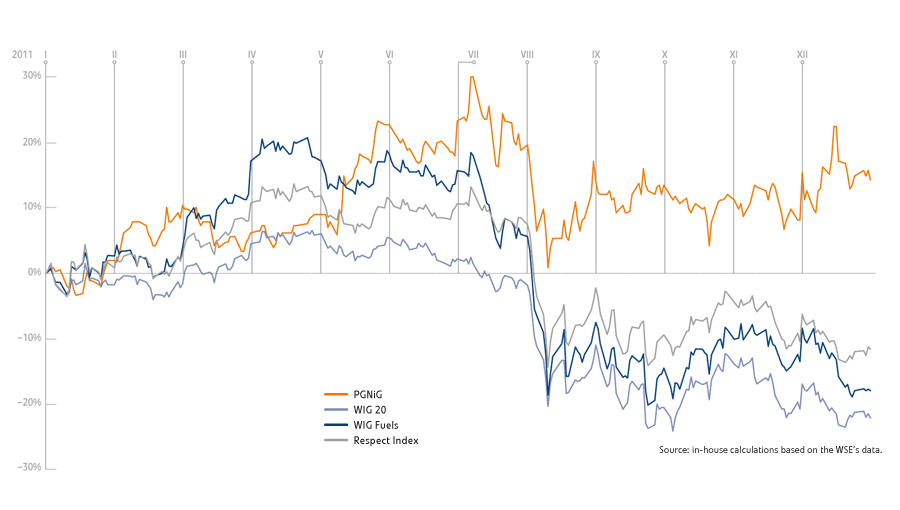

Price Performance of the PGNiG Stock

Throughout the year, PGNiG shares traded within the PLN 3.45–4.64 band. The strongest increases in the share price were driven by the Q1 results, which outperformed the analysts’ consensus estimations, and also followed the approval of the gas fuel tariff increase in June 2011. These were shortly followed by sharp decline of the share price caused by the macroeconomic environment and the downturn seen on the global markets in July and August.

In such difficult conditions, further exacerbated by crude price increases and the weakening of the Polish złoty against the US dollar, the rate of return on PGNiG shares turned out to be one of the highest among companies included in the WIG20 index. In 2011, the rate of return on the PGNiG shares was 14.3%, and including dividend income (PLN 0.12 per share) – 17.6%. The WIG index fell by nearly 21% in the same period. The rate of return on the investment in PGNiG shares for investors who bought the shares at the issue price in 2005 had reached 36.9% by the end of 2011.

| Value/price as at Dec 31 2010 |

2011 high | 2011 low | Value/price as at Dec 31 2011 |

PGNiG’s weight in the index as at Dec 31 2011 |

|

|---|---|---|---|---|---|

| Source: the WSE | |||||

| WIG | 47,490 | 50,372 | 36,549 | 37,595 | 3,2% |

| WIG20 | 2,744 | 2,933 | 2,090 | 2,144 | 4.2% |

| WIG-Fuels | 3,079 | 3,776 | 2,499 | 2,568 | 31.6% |

| Respect Index | 2,259 | 2,577 | 1,944 | 2,005 | 7.79% |

| PGNiG SA | 3.57 zł | 4.64 zł | 3.45 zł | 4.08 zł | – |

| Rate of return 2008 | Rate of return 2009 | Rate of return 2010 | Rate of return2011 | Rate of return since PGNiG’s IPO | |

|---|---|---|---|---|---|

| Source: the WSE | |||||

| 1 Computed in relation to the reference value of the index (reference date: December 31st 2005). | |||||

| 2 Computed in relation to the reference value of the index (reference date: December 31st 2008). | |||||

| 3 In relation to the issue price of PLN 2.98, the rate of return on PGNiG shares since the IPO stands at 36.9%. | |||||

| WIG | -51.1% | 46.9% | 18.8% | -20.8% | 13.2% |

| WIG20 | -48.2% | 33.5% | 14.9% | -21.8% | -12.7% |

| WIG-Fuels | -46.8% | 28.9% | 26.4% | -18.5% | -27.9%1 |

| Respect Index | n/a | 70.9%2 | 32.2% | -12.9% | 100.5%2 |

| PGNiG | -29.4% | 5.3% | -5.8% | 14.3% | 7.1%3 |